Social Security is a major unfunded liability. Younger generations are skeptical that Social Security will not support them when they reach retirement age. You need to know seven things about the looming Social Security crisis.

“Social Security is a secure way to find great pleasure in being terribly decieved.” – Ernie J Zelinski

The Looming Social Security Crisis

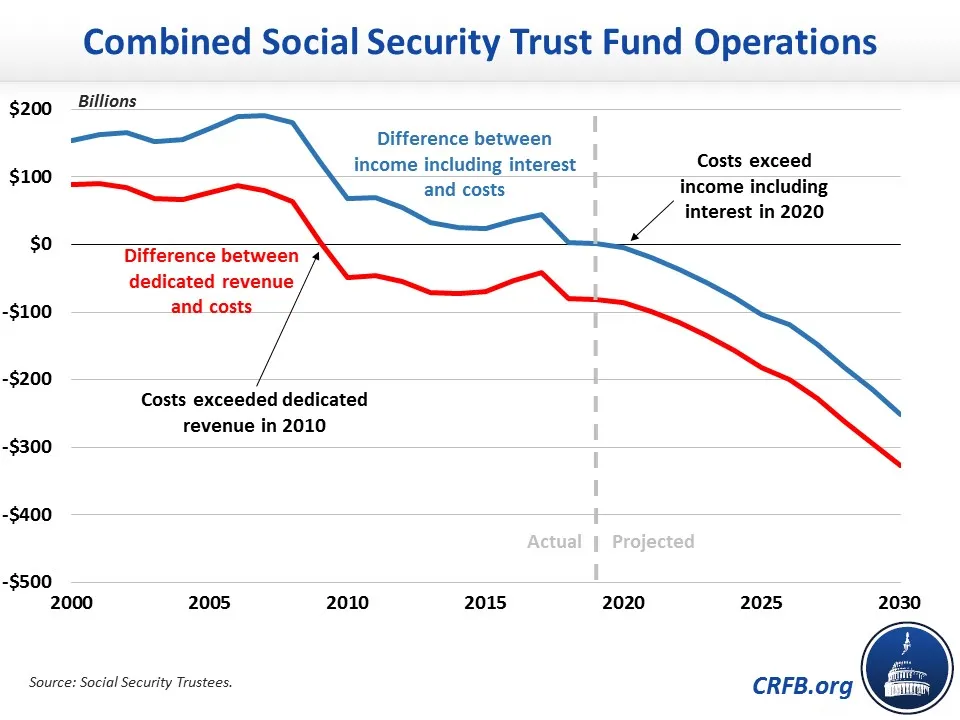

The final year that Social Security had a surplus in funds was 2009. That was fifteen years ago. The program has continued operating on a cash-flow deficit since 2010.

The Social Security Trustees project a $1.8 trillion cash-flow deficit by 2030, requiring Social Security to reduce its trust fund reserves to $864 billion.

Due to continual optimism, financial mismanagement, and positive spin, people may believe they will still receive Social Security when they retire. However, Millennials and younger generations are skeptical that they will receive Social Security.

Are younger people correct in their pessimism? Or is everything rosy? The Social Security Trustees’ reports spin a positive message even though the information and data are very sickly upon closer inspection.

2022 Social Security Trustees’ Report

To make matters even worse, the Social Security Administration has admitted that It will run out of funds by 2034. However, that was before the COVID-19 pandemic, which caused Social Security to dip into more of its funds.

Now, the Social Security and Medicare Board of Trustees projects the “cost of both programs [Social Security and Medicare] will grow faster than gross domestic product (GDP) through the mid-2030s primarily due to the rapid aging of the U.S. population.”

This is a result of an aging population. The demographic issue is that not enough people are working or being born to cover the cost of Social Security.

The Bipartisan Policy Center now projects that Social Security will likely be depleted by 2028.

That is only four years away.

Source: Secure Single created this meme using imgflip.

2023 Social Security Trustees’ Report

According to the Social Security Trustees’ 2023 annual report, the social program will have a cashflow deficit of $119 billion.

Social Security continues to deal with a shortfall in long-term cash flow due to the aging population.

Unsurprisingly, Social Security’s financial health continues to decline. The Social Security Trustees estimate that the trust funds will be insolvent by 2033. That means Social Security is only nine years away from insolvency. Once Social Security is officially insolvent, retirees will experience a 20% cut in benefits received.

How would you feel knowing that the money that was directly taken from your monthly paycheck that you were promised was reduced or eliminated?

1. Dipping Into Trust Funds Reserves

Social Security began dipping into its trust fund reserves in 2020. The trust fund reserves are estimated to be depleted by 2035. The bigger issue is that Social Security will become insolvent by 2033.

The Social Security trust funds consist of money the government collects from payroll taxes, which it then deposits into accounts that pay for disability, retirement, and survivor benefits.

Budgeting and managing money are foundational concepts in personal finance. However, the Social Security program missed that crucial financial lesson. Since 2010, Social Security’s payouts have exceeded the revenue it brings in from taxes.

A person who works for a business would be in debt. However, the government gets a pass when it does the same thing.

The government gets a notable exception because taxpayers fund it. Taxpayers are happy to believe they will receive their promised benefits from the government.

Despite the positive messaging from politicians, the numbers continue to worsen. Other trends continue to be in motion that go against Social Security.

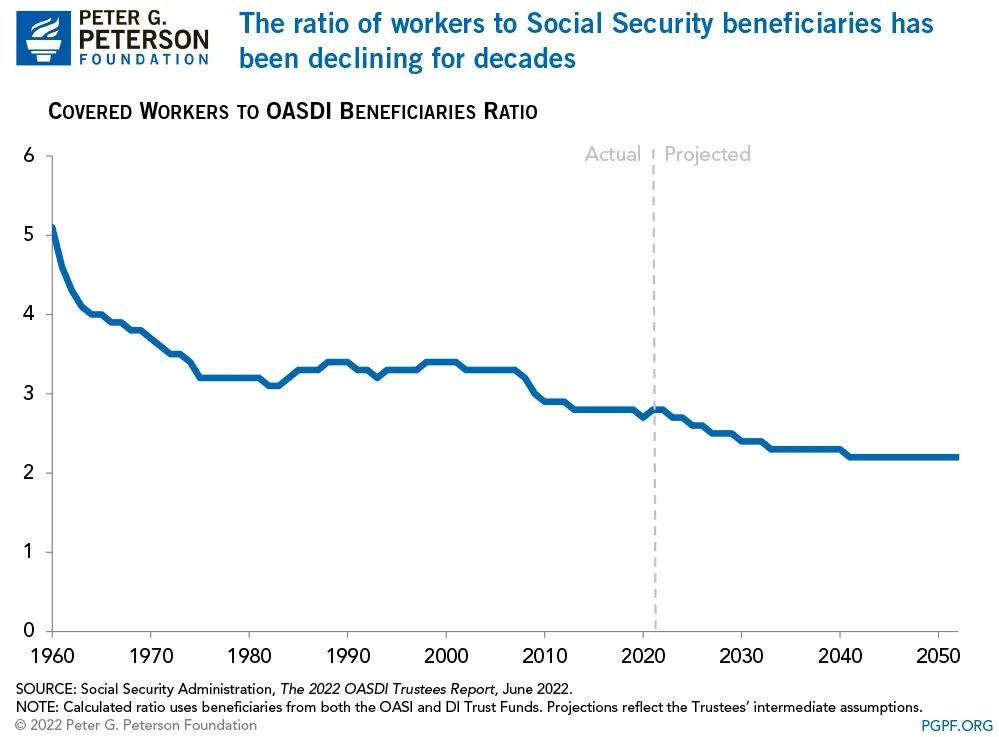

2. Workers Ratio To Social Security Beneficiaries

The Social Security beneficiaries to workers ratio has been declining for decades, adding to the financial difficulties. This trend continues, and it does not bode well for Social Security.

Source: Peter G. Peterson Foundation

Fewer people are now working and paying payroll taxes due to the rise of freelancing and contract work. Freelancers and contract workers do not contribute to payroll taxes. The client pays them directly on a freelancing site, or the money is sent directly to their bank account or a money app such as PayPal or Venmo.

3. Aging Population

Baby boomers are reaching retirement age to receive Social Security. This means they are expecting Social Security to be there for them. They have paid into it throughout their lifetime. They believe they must receive it as a retirement benefit because they paid for it through payroll taxes.

Generations X and younger are more skeptical. Many doubt that they will not receive it once they reach retirement age.

People’s loss of confidence in receiving Social Security is not a generational problem. It is a government problem. The government is not providing solutions to make younger people confident that it will be there for them.

4. Demographic Crisis

The demographic crisis is that population growth in the United States has flatlined. Americans are living longer, which means that Social Security will have to be paid out longer to recipients.

The problem is that older people will begin to draw from those benefits. Social Security’s benefits are running dry due to America’s demographic crisis.

President George W. Bush summarized this problem in his State of the Union Address in 2005:

“In today’s world, people are living longer and, therefore, drawing benefits longer. And those benefits are scheduled to rise dramatically over the next few decades. And instead of sixteen workers paying in for every beneficiary, right now it’s only about three workers. And over the next few decades that number will fall to just two workers per beneficiary. With each passing year, fewer workers are paying ever-higher benefits to an ever-larger number of retirees.”

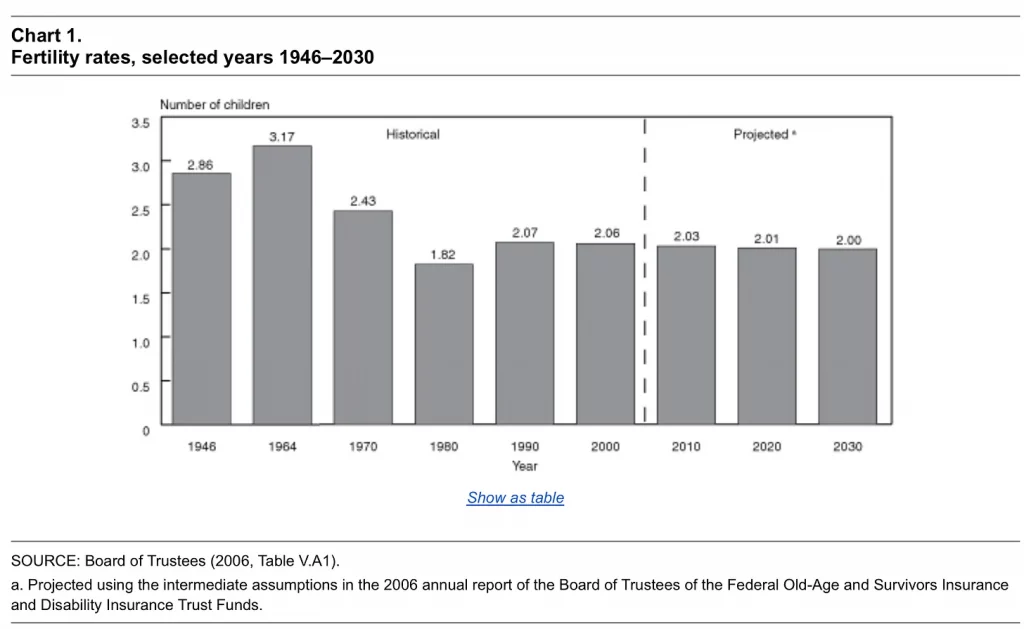

Not only are people living longer, but the number of children born has fallen since the Baby Boom. During the Baby Boom, the average birth rate was 3.17 children per woman. That number has dropped nearly in half, creating a fertility crisis.

Source: Social Security Office of Policy

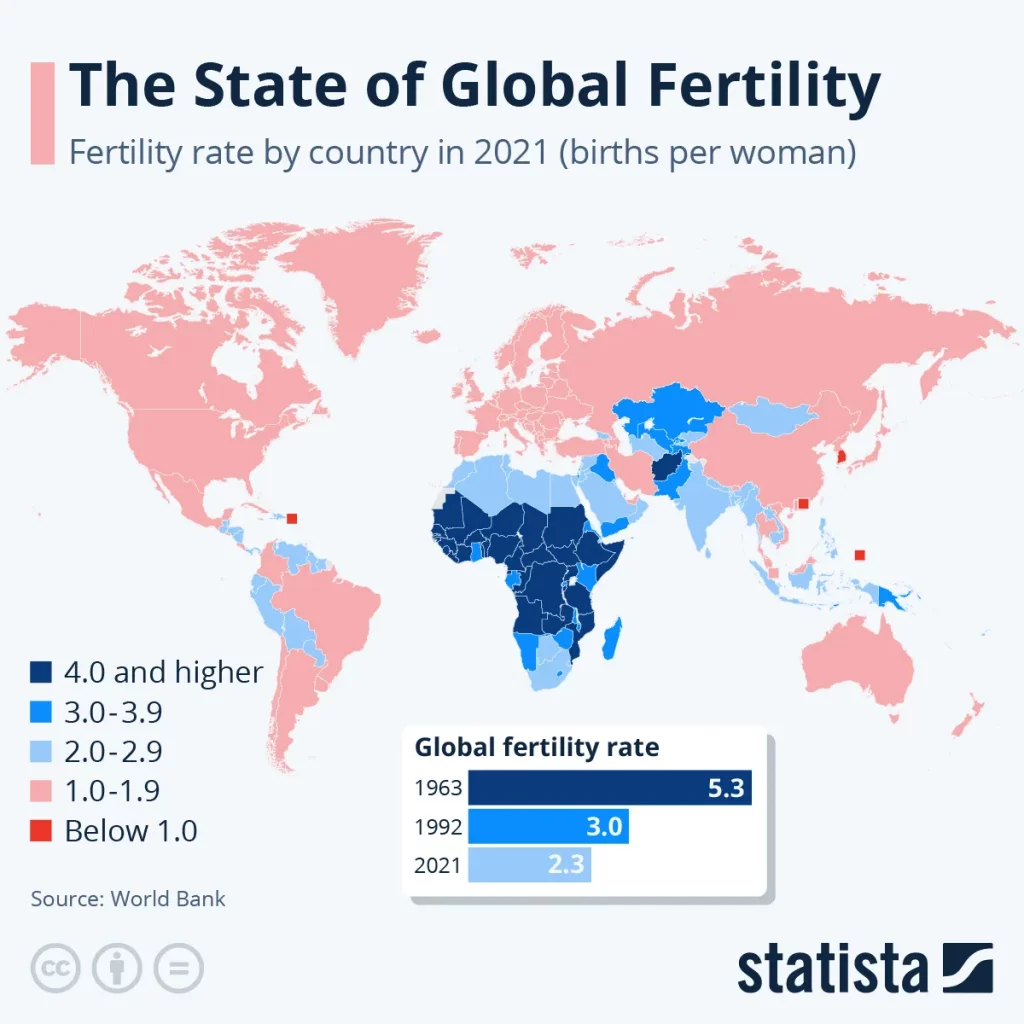

5. Fertility Crisis

People are staying single longer, not marrying, and not having children. With more people delaying marriage and having children, it means that the United States is failing to meet the minimum threshold of two children per woman.

The average birth rate per woman in the United States is 1 to 1.9. The fertility crisis plays a critical role in the Social Security crisis.

The demographic crisis for Social Security means that not enough people are contributing to the program to keep it solvent.

Even if the government raises payroll taxes, it will not make a difference. Social Security will remain unfunded. The fertility crisis will likely continue since it has become trendy not to have children.

More young people are choosing to be childless or child-free.

Source: Statista

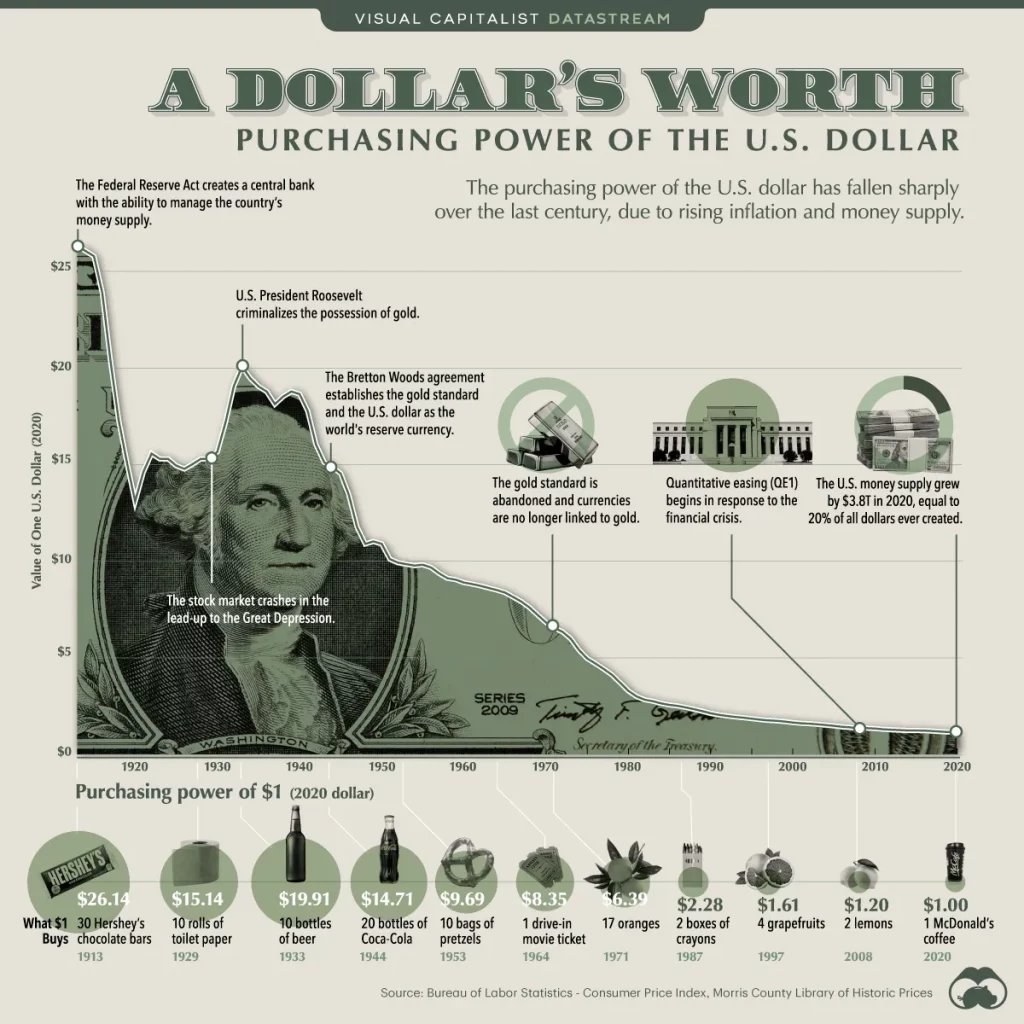

6. Dollar Devaluation

The other coming crisis is the devaluation of the dollar. Fiat currencies throughout history have returned to their intrinsic value of zero. Currencies only have value as long as people have confidence in the currency and central banks do not abuse their powers by inflating away the currency’s value.

Today, people and countries continue to have confidence in the dollar. The only question is, how much longer will that last? China is selling its bonds.

The Federal Reserve continues to be loose with money through quantitative easing (QE). QE expands the monetary supply, creating inflation and devaluing the dollar.

Source: Visual Capitalist

7. Young People Believe They Will Not Receive Social Security

Millennials and younger believe that they will not receive Social Security once they reach retirement age. They view Social Security as a program that only Baby Boomers will benefit from.

It is ultimately a question of how long the government can continue kicking the can down the road. The Federal Reserve could print money (QE) to cover the costs. The problem is that it would increase inflation by expanding the monetary supply. That would be detrimental to retirees and people who are working.

Government Solutions

There are some solutions the movement could implement to try to resolve Social Security’s coming insolvency.

The government could increase payroll taxes. However, the financial consequence is that you earn less money from each paycheck to save, invest, and put into other retirement accounts.

The government could raise the retirement age when people receive Social Security. However, this is not a politically viable option. Politicians of both parties know that it would be political suicide. People want and expect the benefits that the government promised them.

France raised the retirement age, which resulted in protests.

Why would it change if the government failed to budget for Social Security properly? Increasing payroll taxes will not help resolve this problem. Decreased government spending is the only solution if the government wants to maintain the program. All of the other solutions are merely band-aids on an open wound that has become so bad that the leg now needs to be amputated.

Another problem with the government’s efforts to resolve the Social Security crisis will continue to worsen inflation and devalue the dollar. This is because it will continue raising the government’s deficit and spending programs, contributing to inflation.

Government deficits and spending contribute to inflation. This means that even if you receive Social Security, the money will not go as far.

Summary

I do not mean to sound alarmist or to fearmonger. I am just stating the economic reality of the state of Social Security. It is not rosy. I am presenting you with a realistic analysis of the state of Social Security and the multiple crises playing against the positive messaging from politicians, the media, and the Social Security Trustees’s report.

You have no choice but to contribute to Social Security since payroll taxes directly deduct it from your wages. However, it may be prudent to consider other retirement planning strategies.