Social Security is a major unfunded liability. Younger generations are skeptical that Social Security will not support them when they reach retirement age. You need to know seven things about the looming Social Security crisis.

“Social Security is a secure way to find great pleasure in being terribly decieved.” – Ernie J Zelinski

The Looming Social Security Crisis

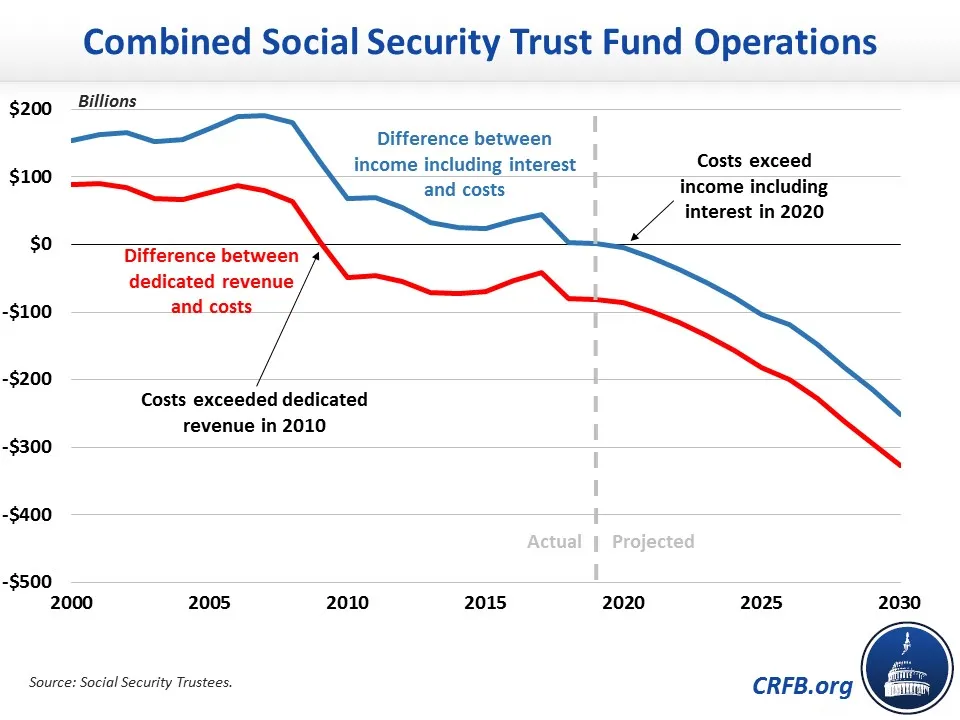

The final year that Social Security had a surplus in funds was 2009. That was fifteen years ago. The program has continued operating on a cash-flow deficit since 2010.

The Social Security Trustees project a $1.8 trillion cash-flow deficit by 2030, requiring Social Security to reduce its trust fund reserves to $864 billion.

Due to continual optimism, financial mismanagement, and positive spin, people may believe they will still receive Social Security when they retire. However, Millennials and younger generations are skeptical that they will receive Social Security.

Are younger people correct in their pessimism? Or is everything rosy? The Social Security Trustees’ reports spin a positive message even though the information and data are very sickly upon closer inspection.

2022 Social Security Trustees’ Report

To make matters even worse, the Social Security Administration has admitted that It will run out of funds by 2034. However, that was before the COVID-19 pandemic, which caused Social Security to dip into more of its funds.

Now, the Social Security and Medicare Board of Trustees projects the “cost of both programs [Social Security and Medicare] will grow faster than gross domestic product (GDP) through the mid-2030s primarily due to the rapid aging of the U.S. population.”

This is a result of an aging population. The demographic issue is that not enough people are working or being born to cover the cost of Social Security.

The Bipartisan Policy Center now projects that Social Security will likely be depleted by 2028.

That is only four years away.

Source: Secure Single created this meme using imgflip.

2023 Social Security Trustees’ Report

According to the Social Security Trustees’ 2023 annual report, the social program will have a cashflow deficit of $119 billion.

Social Security continues to deal with a shortfall in long-term cash flow due to the aging population.

Unsurprisingly, Social Security’s financial health continues to decline. The Social Security Trustees estimate that the trust funds will be insolvent by 2033. That means Social Security is only nine years away from insolvency. Once Social Security is officially insolvent, retirees will experience a 20% cut in benefits received.

How would you feel knowing that the money that was directly taken from your monthly paycheck that you were promised was reduced or eliminated?

1. Dipping Into Trust Funds Reserves

Social Security began dipping into its trust fund reserves in 2020. The trust fund reserves are estimated to be depleted by 2035. The bigger issue is that Social Security will become insolvent by 2033.

The Social Security trust funds consist of money the government collects from payroll taxes, which it then deposits into accounts that pay for disability, retirement, and survivor benefits.

Budgeting and managing money are foundational concepts in personal finance. However, the Social Security program missed that crucial financial lesson. Since 2010, Social Security’s payouts have exceeded the revenue it brings in from taxes.

A person who works for a business would be in debt. However, the government gets a pass when it does the same thing.

The government gets a notable exception because taxpayers fund it. Taxpayers are happy to believe they will receive their promised benefits from the government.

Despite the positive messaging from politicians, the numbers continue to worsen. Other trends continue to be in motion that go against Social Security.

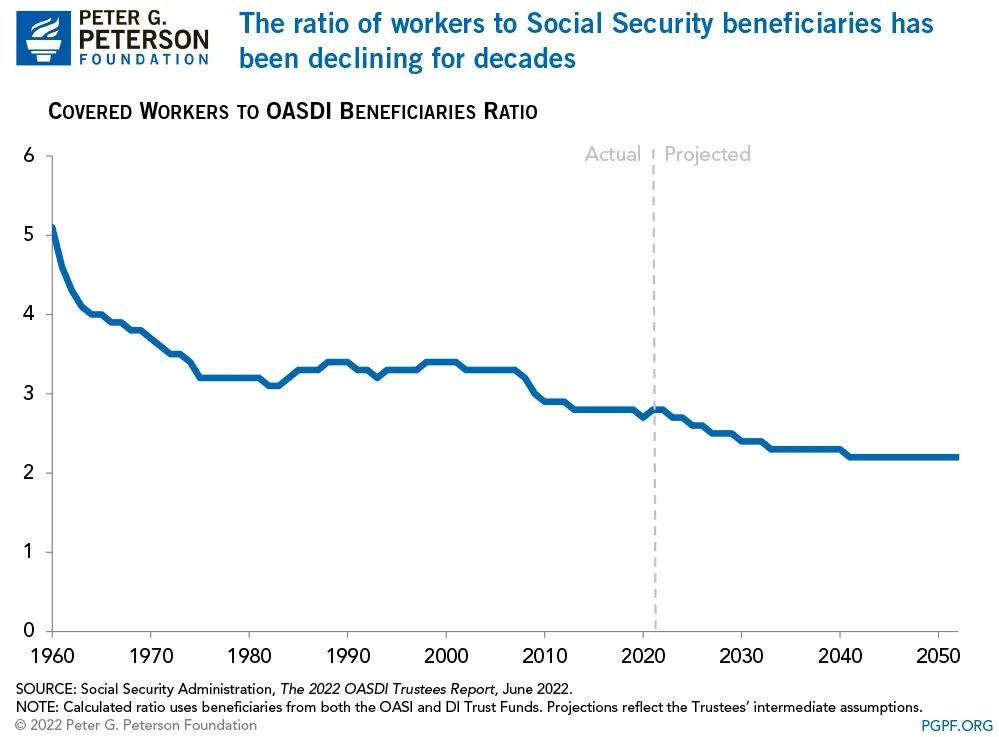

2. Workers Ratio To Social Security Beneficiaries

The Social Security beneficiaries to workers ratio has been declining for decades, adding to the financial difficulties. This trend continues, and it does not bode well for Social Security.

Source: Peter G. Peterson Foundation

Fewer people are now working and paying payroll taxes due to the rise of freelancing and contract work. Freelancers and contract workers do not contribute to payroll taxes. The client pays them directly on a freelancing site, or the money is sent directly to their bank account or a money app such as PayPal or Venmo.

3. Aging Population

Baby boomers are reaching retirement age to receive Social Security. This means they are expecting Social Security to be there for them. They have paid into it throughout their lifetime. They believe they must receive it as a retirement benefit because they paid for it through payroll taxes.

Generations X and younger are more skeptical. Many doubt that they will not receive it once they reach retirement age.

People’s loss of confidence in receiving Social Security is not a generational problem. It is a government problem. The government is not providing solutions to make younger people confident that it will be there for them.

4. Demographic Crisis

The demographic crisis is that population growth in the United States has flatlined. Americans are living longer, which means that Social Security will have to be paid out longer to recipients.

The problem is that older people will begin to draw from those benefits. Social Security’s benefits are running dry due to America’s demographic crisis.

President George W. Bush summarized this problem in his State of the Union Address in 2005:

“In today’s world, people are living longer and, therefore, drawing benefits longer. And those benefits are scheduled to rise dramatically over the next few decades. And instead of sixteen workers paying in for every beneficiary, right now it’s only about three workers. And over the next few decades that number will fall to just two workers per beneficiary. With each passing year, fewer workers are paying ever-higher benefits to an ever-larger number of retirees.”

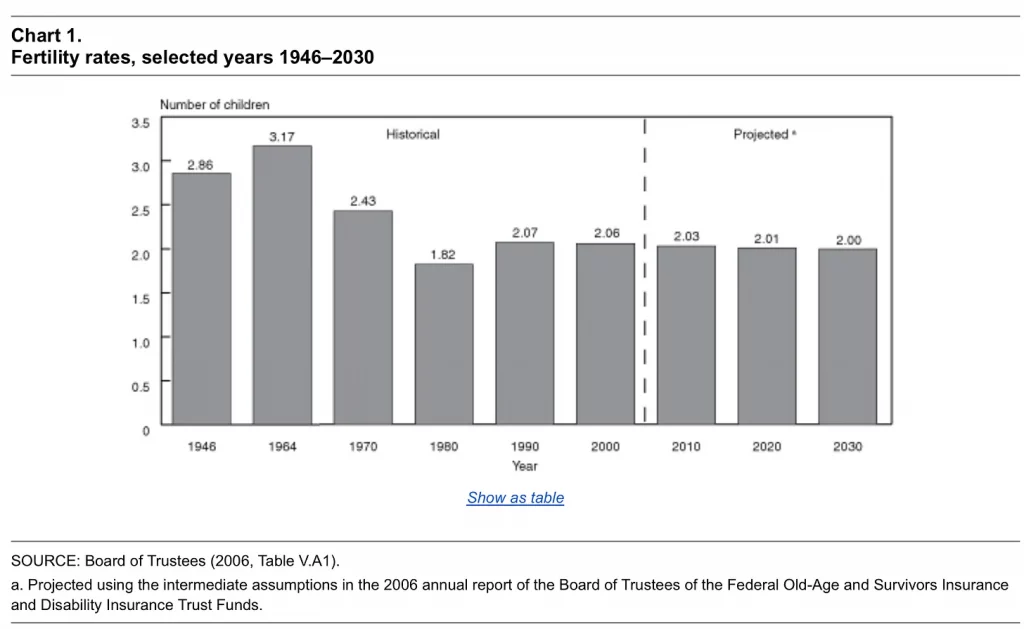

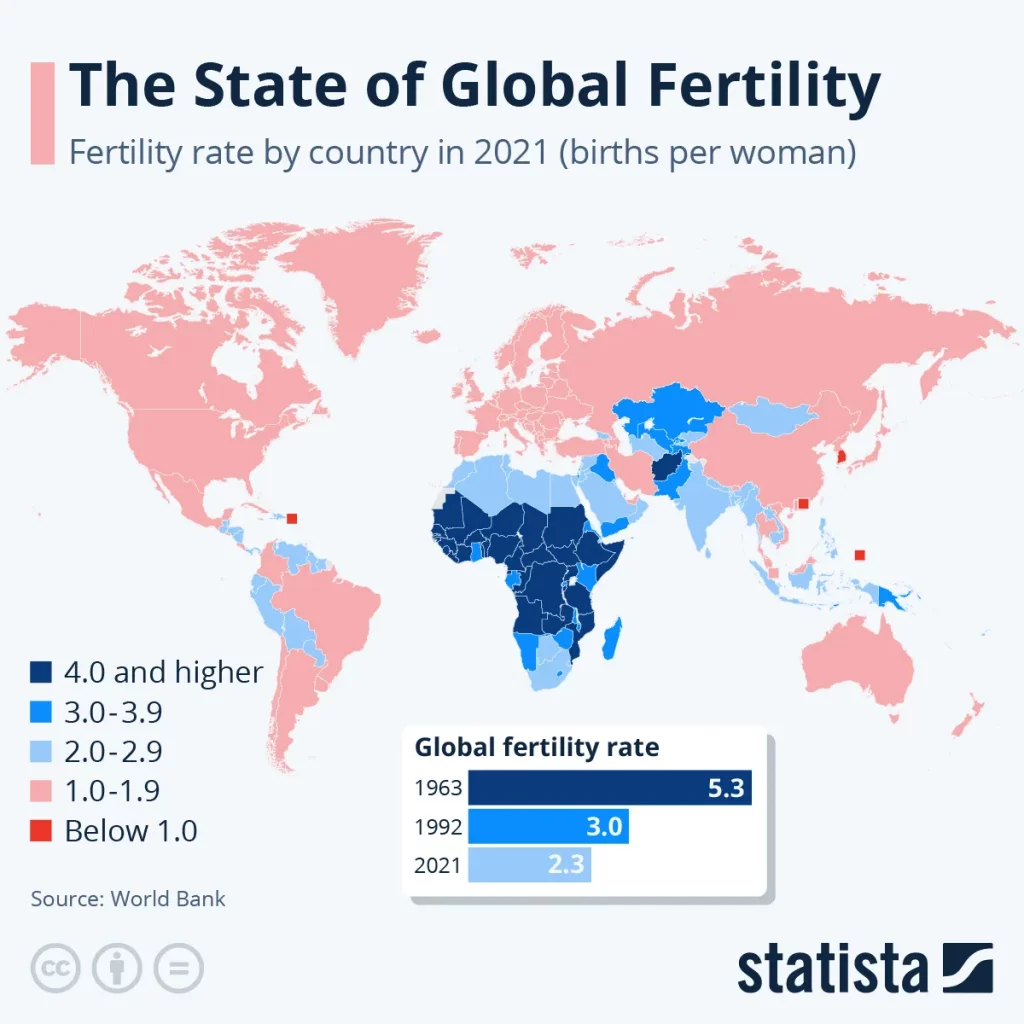

Not only are people living longer, but the number of children born has fallen since the Baby Boom. During the Baby Boom, the average birth rate was 3.17 children per woman. That number has dropped nearly in half, creating a fertility crisis.

Source: Social Security Office of Policy

5. Fertility Crisis

People are staying single longer, not marrying, and not having children. With more people delaying marriage and having children, it means that the United States is failing to meet the minimum threshold of two children per woman.

The average birth rate per woman in the United States is 1 to 1.9. The fertility crisis plays a critical role in the Social Security crisis.

The demographic crisis for Social Security means that not enough people are contributing to the program to keep it solvent.

Even if the government raises payroll taxes, it will not make a difference. Social Security will remain unfunded. The fertility crisis will likely continue since it has become trendy not to have children.

More young people are choosing to be childless or child-free.

Source: Statista

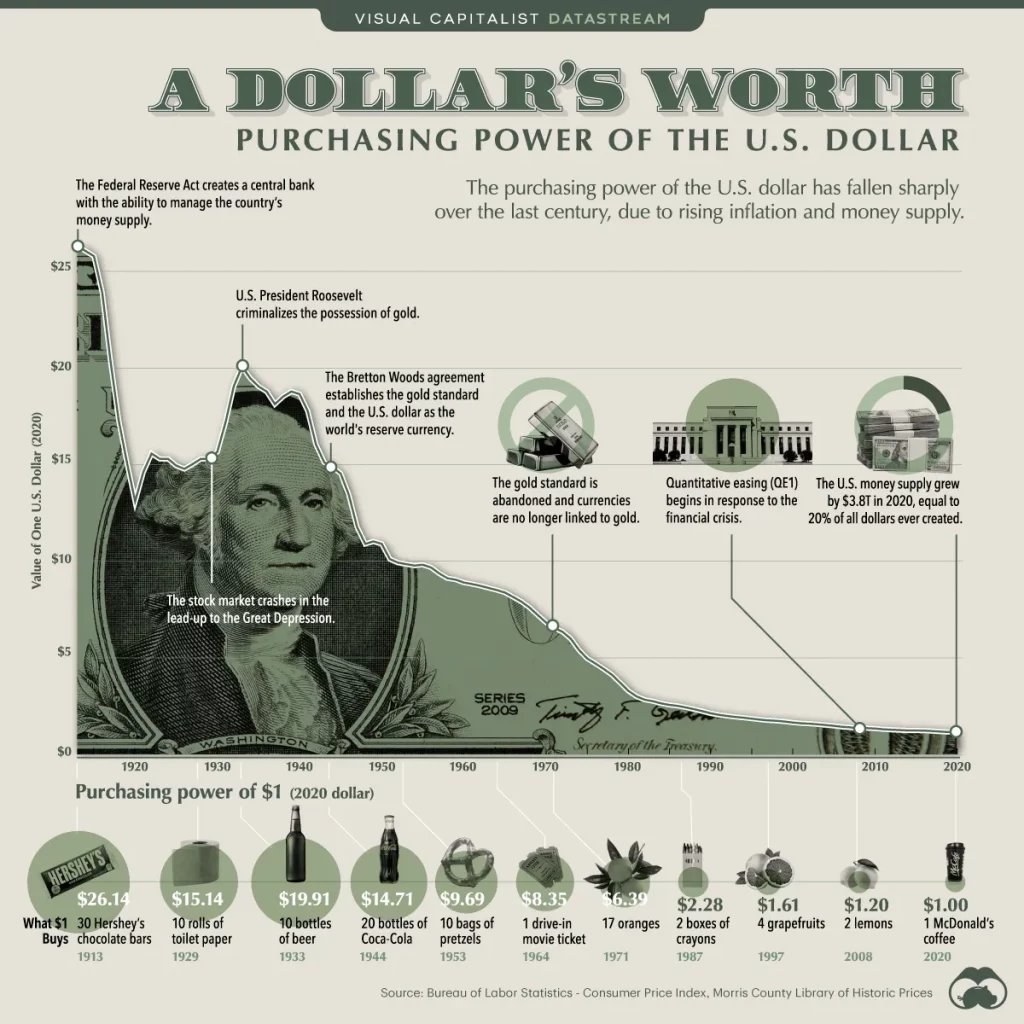

6. Dollar Devaluation

The other coming crisis is the devaluation of the dollar. Fiat currencies throughout history have returned to their intrinsic value of zero. Currencies only have value as long as people have confidence in the currency and central banks do not abuse their powers by inflating away the currency’s value.

Today, people and countries continue to have confidence in the dollar. The only question is, how much longer will that last? China is selling its bonds.

The Federal Reserve continues to be loose with money through quantitative easing (QE). QE expands the monetary supply, creating inflation and devaluing the dollar.

Source: Visual Capitalist

7. Young People Believe They Will Not Receive Social Security

Millennials and younger believe that they will not receive Social Security once they reach retirement age. They view Social Security as a program that only Baby Boomers will benefit from.

It is ultimately a question of how long the government can continue kicking the can down the road. The Federal Reserve could print money (QE) to cover the costs. The problem is that it would increase inflation by expanding the monetary supply. That would be detrimental to retirees and people who are working.

Government Solutions

There are some solutions the movement could implement to try to resolve Social Security’s coming insolvency.

The government could increase payroll taxes. However, the financial consequence is that you earn less money from each paycheck to save, invest, and put into other retirement accounts.

The government could raise the retirement age when people receive Social Security. However, this is not a politically viable option. Politicians of both parties know that it would be political suicide. People want and expect the benefits that the government promised them.

France raised the retirement age, which resulted in protests.

Why would it change if the government failed to budget for Social Security properly? Increasing payroll taxes will not help resolve this problem. Decreased government spending is the only solution if the government wants to maintain the program. All of the other solutions are merely band-aids on an open wound that has become so bad that the leg now needs to be amputated.

Another problem with the government’s efforts to resolve the Social Security crisis will continue to worsen inflation and devalue the dollar. This is because it will continue raising the government’s deficit and spending programs, contributing to inflation.

Government deficits and spending contribute to inflation. This means that even if you receive Social Security, the money will not go as far.

Summary

I do not mean to sound alarmist or to fearmonger. I am just stating the economic reality of the state of Social Security. It is not rosy. I am presenting you with a realistic analysis of the state of Social Security and the multiple crises playing against the positive messaging from politicians, the media, and the Social Security Trustees’s report.

You have no choice but to contribute to Social Security since payroll taxes directly deduct it from your wages. However, it may be prudent to consider other retirement planning strategies.

The views expressed in this article are the author’s opinions and do not necessarily reflect the views of Secure Single. It is intended for informational and educational purposes only and is not investment, financial, or legal advice. Consult with a financial or legal professional before making investment or legal decisions. James Bollen is the author of Thriving Solo: How to Flourish and Live Your Perfect Life (Without A Soulmate). It is now available in paperback and Kindle on Amazon.

Sex is an integral part of human life, but it has become overly idolized in society. It is time to take back control of your life and embrace a sexless lifestyle. Here are ten compelling reasons why you should consider this option.

The Empowerment Of Choosing A Sexless Lifestyle

No Distractions Or Addictions

Are you tired of being distracted by romantic and erotic relationships? These relationships can take away your valuable time, energy, and attention. And what if the relationship doesn’t work out? You are left with even more pain and heartache.

But guess what? You don’t have to be in a relationship if you’re not ready or don’t want to be. Choosing to live a sexless life can do wonders for your self-improvement journey. Without the distractions or addictions of romantic relationships, you can focus on yourself, your goals, and your passions.

So, take control of your life and say no to these distractions. Choose to prioritize self-improvement by living a sexless life, either temporarily or permanently. It’s time to focus on what really matters – you.

Internal Validation

Internal validation and external validation are two opposing concepts. External validation relies on being validated by others, such as receiving likes and followers on social media or owning the latest trendy product.

On the other hand, internal validation is about goal-setting and working hard to achieve them. Accomplishing these goals helps build self-confidence, a crucial aspect of personal success.

Goal Setting

Setting goals is critical to measuring success. You can use the SMART goals system. The acronym stands for:

- Specific

- Measurable

- Achievable

- Relevant

- Time-bound

Following this strategy makes you more likely to accomplish your goals.

Self-Discipline

Self-discipline is crucial for a fulfilling life. Practicing self-discipline and avoiding distractions like social media, sex, news, or politics is vital for your well-being.

Taking responsibility for your actions and being mindful of your decisions can positively impact you. Every decision you make has the potential to affect us positively or negatively. You must practice discipline and act intentionally to achieve your goals.

Self-Control

Self-control is useful when controlling your urges and reaching your goals. Learning self-control is essential, not letting sex or romantic relationships control your life. Instead of engaging in constant dating, watching porn every night, or browsing cam sites regularly, it’s best to practice self-control.

By practicing self-control, you can use your valuable time and attention better and channel them towards achieving your goals.

Self-Learning

Self-learning is critical to achieving personal success. The education system teaches you how to be a good employee but does not teach you critical thinking and life skills.

Self-education is power. You can continue to dive as deep into a topic you want to learn more about. Today, you watch videos, read blog articles, or purchase a digital course on a topic.

Only education with application is valuable. What you are teaching yourself must improve your life in some way. Self-study is the best way to learn applicable skills. You know the skills you need to learn to advance your career, switch fields, or raise your income.

Discover Your Obsession

Instead of fixating on someone of the opposite sex, take some time to discover your true obsession. Your obsession is likely what you are meant to do, giving you a sense of inner peace and purpose when engaging in it.

Once you have identified your obsession, focus on developing the skills related to it and turning it into a career.

Master Your Skills

Discovering your skills in your twenties is crucial to achieving success. Distractions may lead you to believe you can do something you’re not proficient at, but this will only waste your valuable time and delay your income.

For instance, I began a YouTube channel to make money online from advertising revenue. However, I lack the charisma and fun personality necessary to succeed on video platforms. After making a few hundred videos, I accepted that I am better at creating written content than video content. Know and play to your strengths and learn from your mistakes.

Mastering a core skill in something you enjoy doing is the key to success. Expanding to complementary skills only enhances your abilities, making you more valuable in the job market. Having multiple skills in the same niche keeps you on the path to excellence, and it is a sure way to stand out from the crowd.

Increase Your Income

It is essential to constantly work on increasing your income. The money you earn loses its value each month due to inflation. Even at a low rate of 2% inflation, you are losing money. Over a year, your money loses 24% due to compounding inflation.

More than saving money is needed as inflation eats away at your money. To combat this, you must find ways to raise your yearly income. Some options are investing in the stock market, becoming a landlord, purchasing a house (as long as the market does not fall), or starting an online business. You can even combine these options, such as investing in the stock market and reinvesting profits to start an online business.

If functioning correctly, a business can generate a higher return on investment than certain stocks. However, you must determine how to monetize your business by selling products or services.

By combining investments with a business, you have a greater chance of betting on the actual inflation rate. Any income you make beyond the inflationary rate can help you build wealth, which you can reinvest into other asset classes.

To build personal wealth: invest, reinvest, and repeat. Once you have wealth, preserve it.

Freedom

Investing time and money in dating might be tempting if you are single. However, you could be missing out on the freedom of being single. Embrace this freedom to focus on yourself, achieve your goals, and become the best version of yourself without any distractions.

With the freedom of being single, you can spend quality time with friends, family, and your community. You can also learn how to use your professional connections to advance your career or grow your business.

Remember your health. Focusing on fitness and nutrition can make you happier, healthier, and more confident.

By directing your time, attention, and energy toward your personal and professional goals, you can make them a reality. Additionally, wisely invest your finances to build wealth and secure your future.

The choice is yours—will you take advantage of this freedom or waste it on another bad romantic relationship?

Remember, improving yourself and achieving your goals is always possible. Make the most of your single life and become the best version of yourself.

Summary

Living a sexless lifestyle can help you achieve success. By practicing self-control, you can channel your energy into accomplishing great things. Don’t let societal pressures dictate your life. Take control and invest in yourself.

The views expressed in this article are the author’s opinions and do not necessarily reflect the views of Secure Single. It is intended for informational and educational purposes only and is not investment, financial, or legal advice. Consult with a financial or legal professional before making investment or legal decisions. James Bollen is the author of Thriving Solo: How to Flourish and Live Your Perfect Life (Without A Soulmate). It is now available in paperback and Kindle on Amazon.

Do you need to go to college? Will going into debt for college help your future? Is college worth it? Here is a look at why attending college may not be worth it.

Is College Worth It?

Financial Considerations

The cost of obtaining a college degree is a primary source of financial stress for many students. It burdens them with debt and prevents them from saving and investing for their future. In fact, according to Statista, the average cost of attending a four-year university ranges from $24,000 to $60,000 per year. Students typically will spend anywhere from $100,000 to $250,000 to earn a four-year degree.

Furthermore, research by Research.com shows that college costs have increased by a staggering 143% for full-time students since 1963. This alarming fact indicates that the burden of student debt will only worsen. According to The College Investor, the average student loan debt balance in 2024 was $37,718.

Student debt is a typical unsecured debt many Americans have. Many will continue to pay off their student loans after graduation. This debt can hinder your ability to save and invest money.

Consider the critical long-term financial impacts of attending college and accumulating debt. You can explore alternative options to avoid taking on too much debt and compromising your financial well-being.

Educational Considerations

When it comes to education, we need to be smart about how we invest our money. College education is often seen as the gold standard, but is it really worth it? Let’s face it: college is just a more advanced version of high school. Students learn from textbooks, take quizzes and tests, and gain book knowledge that often never translates to practical skills.

Even in specialized fields like information and cybersecurity, most graduate programs offer limited opportunities for hands-on learning, relying instead on outdated textbooks and exams.

The education system only follows one method of learning: reading and exams. There are more effective ways to learn. There are many ways to learn.

The better way to learn is to take digital courses on topics of interest to you. These courses are designed to provide critical information in a condensed format so you can complete them in a few days. Unlike college courses, digital courses focus on practical skills you can apply in the real world.

The best part? Digital courses can provide a certificate showing that you completed the course. You can then add the digital course’ certificate to your LinkedIn profile and resume, providing tangible evidence of your skills and knowledge.

So, before you invest your money in a college education, consider the benefits of digital courses. With digital courses, you can learn practical skills that will help you succeed in the real world, all in a fraction of the time and money it takes to earn a degree.

Lifestyle Considerations

Attending college can lead you towards negative lifestyle habits that can be detrimental to your personal growth. Unfortunately, the college party scene often reinforces these habits, which include excessive drinking, smoking, promiscuity, gambling, and seeking validation from others.

However, there is an alternative. Instead of attending college, you can develop positive lifestyle habits that benefit your overall well-being. Doing so may make you more successful than your peers who decided to attend college. You can start working on these habits while working or starting your own business, allowing you to build a foundation for a fulfilling and successful life.

Do not let college dictate your life choices and habits. Choose the path less traveled and focus on developing positive habits that will benefit you in the long run. Doing so may unlock your full potential and help you discover success beyond your wildest dreams.

Will College Help You To Get A Career?

It is a common misconception that a college degree is the key to landing your dream job. However, the reality is that many college-educated individuals end up working in entry-level retail jobs.

I have had to work primarily in retail and merchandising jobs, even though I attended college and graduate school. No employer would hire me because I lacked the proper work experience, and they did not care that I spent nearly a decade in the higher education system.

Your work experience, not your academic background, truly matters to companies. Having hands-on experience in your field can make you a more valuable candidate than someone with a degree but no practical experience.

Do not forget that you can succeed in your career without a college degree. With the right skills and a winning attitude in interviews, you can demonstrate your capabilities and secure the job you want. So do not be discouraged if you do not have a degree—focus on building your skills and experience, and the opportunities will follow.

Dilemma Of Getting A College Degree Versus Work Experience

Choosing between college and work experience can be a daunting decision for young people. While college can provide you with valuable knowledge, many employers now favor candidates with work experience and skills over those with a college degree.

It may be more beneficial to prioritize work experience over earning a college degree. Work experience allows you to gain hands-on experience that employers may require. Studying and acquiring the necessary certifications and skills can make you more competitive and help you work up in a company or industry.

In today’s job market, staying competitive requires acquiring the skills and experience employers value most. You must carefully decide whether attending college or gaining work experience is best to make informed decisions that align with your career goals.

Summary

Is obtaining a college degree worth it? That depends on your career aspirations and whether or not you think it’s worth taking on debt. In some cases, it may not be worth it, as you spend most of your twenties learning theoretical knowledge that is irrelevant to the practical skills needed to secure a job.

The views expressed in this article are the author’s opinions and do not necessarily reflect the views of Secure Single. It is intended for informational and educational purposes only and is not investment, financial, or legal advice. Consult with a financial or legal professional before making investment or legal decisions. James Bollen is the author of Thriving Solo: How to Flourish and Live Your Perfect Life (Without A Soulmate). It is now available in paperback and for the Kindle on Amazon.

The American Dream says that if you work hard enough, a person can make something of themselves. That is true of traditional jobs that exist only in specific sectors today. For everyone else, there are now part-time and dead-jobs in America.

Dead-End Jobs In America

There may still be some traditional jobs that allow a person to work their way up. Those jobs are now mostly only in specific fields. Namely STEM fields. Outside of those areas, part-time and dead-end jobs are now standard.

Most people now work in some sort of retail job. The United States has become a service economy. The FRED says the rise of the service economy is a good thing, even though those jobs pay less than other jobs that require more skill. The job may pay just above minimum wage.

Service jobs often do not pay enough for a person to be able to pay rent and other expenses that are necessary to live. It may or may not provide benefits (most likely not). A person cannot live on that with the rising cost of living. A person will never be able to buy a house working a part-time or retail job in the modern economy. Yet, the St. Louis Fed says that the growth of the service sector is great for the economy!

Dead-end jobs are the new normal. Millennials grew up with dead-end jobs as the standard. Deloitte writes regarding the rise of dead-end jobs. “Today, this model [the traditional career] is being shattered. As research suggests, and as I’ve seen in my career, the days of a steady, stable career are over. Organizations have become flatter and less ladder-like, making upward progression less common (often replaced by team or project leadership).”

The consequence of having less ability to move up in a company is that more people are stuck working entry-level jobs.

Despite attending college and later graduate school, my experience has been working random dead-end jobs. This has become the economic reality for many people. A college degree is no longer a guarantee that a person can get a job in a career that will allow them to work in a company.

Global Competition

Manufacturing jobs have been outsourced. Millennials and Gen Z now must compete on a global scale. Freelance and contract work are more common. Past generations do not have to face the competition to get a job that millennials and younger generations must face.

Previous generations did not face global competition in the workplace. Competition for jobs was only national. Companies can get away with paying employees less for working fewer hours due to job competition. The job does not even need to cover the bills. This is why it is common for a person to work two or three part-time jobs.

Solutions

The solution for Millennials and younger generations is solopreneurship. Entrepreneurship has always been the option to escape the rat race. To escape working a job you hate. In the Internet age, a person can start an online business.

An online business can be focused on one or more of the evergreen niches:

- Health

- Relationships

- Money

In the 21st Century, building a personal brand and a business is more accessible. Create a YouTube or TikTok channel. Start a website or Substack. A business must sell products and services to people. That is the essence of a business. An e-commerce business can sell:

- Physical products

- Digital products

- Coaching and other services

- Subscriptions

- Merchandise

The main reason why many people will not want to start a business is because it requires self-responsibility. The business owner is responsible for working to build revenue streams. Once a company has made enough money, a business owner can hire people to regain the time spent building the business.

Freelancers and contractors are the most cost-effective way of doing this. They are not full-time employees. An online business does not need to pay them benefits that come with a full-time employee. An online business owner can use the trend of part-time and gig work to save money. A business owner can choose to offer full-time work benefits after the business makes a profit, and the founder can consistently take a percentage off the top to pay oneself. That can take years, depending on the business niche and how business-savvy the business owner is starting.

Summary

Part-time and dead-end jobs are more common today. Young people can escape having to work dead-end jobs by accepting self-responsibility and starting their own online business. An online business is an opportunity to build a personal brand and business. A business has always been the way to build wealth since it is a financial asset that allows the business owner to create multiple income streams while enjoying the legal protections of having a business entity.

Views expressed in this article are the author’s opinions and do not necessarily reflect the views of Secure Single. It is intended for informational and educational purposes only. It is not investment, financial, or legal advice. Consult with a financial or legal professional before making an investment or legal decision. James Bollen is the author of Thriving Solo: How to Flourish and Live Your Perfect Life (Without A Soulmate). It is now available in paperback and for the Kindle on Amazon.

Why is personal finance never taught in schools? Why is this critical life skill never taught to people? Why do most people not understand the basics of personal finance? Here is a look at why schools avoid teaching personal finance.

Why Schools Avoid Teaching Personal Finance

The education system has a simple goal. It is not to educate you. It is not meant to develop young people into well-rounded and critical-thinking citizens. It is not to teach the life skills that are needed to make someone successful. The goal of the education system is to dumb people down and to make them into compliant workers for corporations.

This is done by never teaching personal finance in the classroom. If it is discussed at all, it is at a bare minimum. This is because the financial system does not want people to learn the basics of personal finance.

In high school, I was only taught during one class what a certificate of deposit (CD) was and how to write a check. That shows how displaced the education system is from teaching essential life skills to future generations.

The consequence is it makes young people susceptible to going into debt. There are many types of debt: credit cards, mortgages, car loans, medical, and higher education. Debt is a way to control the people. It is a way to ensure that people cannot advance and live a good life.

Once a person is in debt, getting out can be very difficult. This makes it nearly impossible for someone to begin to save, invest, and reach financial freedom. It also makes a person an employee for life. They are indentured to their employer because they must pay off their debt.

The actual reason why schools avoid teaching personal finance is that students must become obedient and unthinking employees to employers.

Taught To Be An Employee, Not An Employer

The education trains young people to become obedient employees. Unthinking people make great employees. They do what they are told. They are unable to think for themselves. They want to clock in and clock out to earn a paycheck simply.

The problem with being an employee is that it is challenging to keep up with inflation and the rising cost of living. An employee can only negotiate so much with an employer for a raise. Employees are replaceable. This is becoming even more evident with artificial intelligence, automation, and technology.

In contrast, an employer is a business owner. A business owner can find ways to increase one’s income by releasing a new product or service. In the Internet Age, a business owner can sell products and services online. There is no longer a need to sell in person. The result is that a business can reach a global audience, not just an audience in one fixed area.

I have noticed this with the book that I self-published on Amazon. I can reach people outside of the United States. This allows me to reach a wider audience of people who may be interested in my book “Thriving Solo: How to Flourish and Live Your Perfect Life (Without A Soulmate),” which is available through Amazon.

Two Options

You have two main choices. Be an employee or be an employer. Not everyone is meant to be a business owner since it requires lots of personal responsibility until the business makes enough money to delegate tasks.

The problem is that employees are limited in how much they can make in their field. Eventually, the peak will be met, where you will reach your maximum earning potential. You will then decide if you are fine where you are or if it may be a good choice to change career paths.

The other option is to become a business owner. You will deal with the struggles of working with freelancers, time management, and other complications. Once the business generates enough revenue and makes a profit, the business owner can delegate tasks to contractors and employees. This allows the business owner to get his time back while continuing to make money.

It is up to you to decide if you are happy being an employee or if you may want to take the risk in solopreneurship.

Secure Single recommends:

-

What Is Antinatalism?

-

An Introduction To Online Safety For Single Women

-

How Being Single Can Save You Money

Summary

Why do schools avoid teaching about personal finance? It is because the education system is a factory. It produces obedient workers for employers, not self-confident and critical thinkers who can start their own businesses. The good news is that you can transition from being an employee to being your own boss. It will just require that you decide to want to commit to making the change.

Views expressed in this article are the author’s opinions and do not necessarily reflect the views of Secure Single. It is intended for informational and educational purposes only. It is not investment or financial advice. James Bollen is the author of Thriving Solo: How to Flourish and Live Your Perfect Life (Without A Soulmate). Now available in paperback and for the Kindle on Amazon. Subscribe to Secure Single’s Substack for free!

Do you need to date? Why not invest in yourself? Why not save money to reach your goals? Here are five ways how being single can save you money.

How Being Single Can Save You Money

Do Not Need To Pay For Dates

There is no need to pay for dates. Dates can range from cheap to expensive. It will depend on your budget and your interest in the other person.

Not dating puts more money into your pocket. You can then save or invest that money.

Time

Staying single and not dating saves you time. Rather than focusing on getting validation from another person, learn to value each moment. Spending time with a significant other or other people is unnecessary.

Solitude helps with creativity, Solitude improves productivity. Solitude can help to reach goals. It just requires you to begin to value your time. Spend your time investing in yourself to find ways to increase your income.

Attention

Be careful of who and what gets your attention. Direct your attention to work on yourself. A significant other can take away your attention. That attention could be better spent on investing in yourself.

There is nothing wrong with not directing your attention to date. You may not be ready to date. Or you may have no interest in dating. It is fine either way. There is nothing wrong with focusing on yourself.

Start to invest in yourself by beginning to know yourself. Knowing one’s strengths and weaknesses is better than always pursuing the next romantic relationship.

Your attention is valuable. Treat it like the critical commodity that it is. Pay attention to who and what gets your attention. Dedicate your attention to self-improvement and learning about personal finance.

Energy

Planning dates and activities with a significant other can take a lot of energy. This also applies to friendships. For introverted people like me, spending with people can be exhausting.

Make a point of getting the most difficult tasks done in the morning. When you have the most energy during the day, direct it to work towards goals that you want to accomplish.

Spend your energy finding ways to build passive income streams instead of finding a significant other.

Invest Money

Rather than spending money on dates or going out, invest money. Investing is about growing money. It is a way to make your money work for you. Common types of investments are the stock market, real estate, and businesses.

Figure out what your strengths are. Find ways to make an income from those skills. Then, direct the income toward an investment. Make it a goal to build passive income streams.

Secure Single recommends:

-

An Introduction To Online Safety For Single Women

-

Debunking The Myth Of The Magical Other

-

15 Habits To Build Wealth For Singles

Summary

There is nothing wrong with being single. Being single can help you to save money. It is a time to learn about oneself. Being single is a time to focus on self-improvement, personal finance, and to become the best version of yourself.

Views expressed in this article are the author’s opinions and do not necessarily reflect the views of Secure Single. It is intended for informational and educational purposes only. It is not investment or financial advice. James Bollen is the author of Thriving Solo: How to Flourish and Live Your Perfect Life (Without A Soulmate). Now available in paperback and for the Kindle on Amazon. Subscribe to Secure Single’s Substack for free!

There are many distractions you can focus on: romantic relationships, politics, and the news. Instead of focusing on external distractions, begin to invest in yourself. Self-investment is the best way to thrive.

7 Types Of Self-Investment

Self-investment means that you invest in yourself. There are many ways to do that:

• Self-education

• Personal finance

• Self-development

• Learn to cook

• Health

• Relationships

• Monetize your passion

Self-Education

Self-education plays a more critical role in one’s life than the education system. Self-study allows a person to learn more about what they find interesting. Self-education is one characteristic of self-made millionaires.

You can become a master of a topic or field through self-study. No fancy overpriced college degree is required.

Related – 12 Reasons Why Young People Should Not Go To College

Personal Finance

Personal finance plays a critical role in people’s daily lives. Master the basics of personal finance before working to move on to more advanced strategies to increase your income. The basics are:

- Stay out of debt

- Live below your means

- Follow a budget

- Spend less money than you make each month

- Save money

- Invest money

- Build an emergency fund

- Find ways to increase your income

- Build passive income streams

Start with the basics. Once the basics are done, focus on more advanced personal fiancé strategies like building passive income streams and starting an online business.

Related – 50/30/20 Budget Versus 60/30/10 Budget

Self-development

Self-development is concerned with working on oneself. Ultimately, each person must decide what is most important to them. A range of skills fall under the category of personal development:

- Hard skills

- Soft skills

- Interpersonal relationships

- Intrapersonal relationship

- Managing money

- Time management

- Develop a growth mindset

- Resiliency

- Mindfulness

- Practice gratitude

Learn To Cook

Learn to cook. Cooking is a way to save money. It is cheaper to make a meal for oneself than go out to eat or buy pre-prepared food. Start to use the kitchen more. Find and make simple recipes. Freeze the leftovers.

Health

Health is critical. There are many reasons to pay attention to personal health. When your health is terrible, you may be unable to work or be productive. Some ways to focus on health are:

- Regularly exercise

- Go to the gym

- Go for a daily walk

- Get enough sleep

- Get exposed to the sunlight for Vitamin D

- Regularly see a doctor

- Follow a healthy diet

- Lose weight

- Autophagy

Relationships

Relationships play a vital role in one’s life. The range of relationships include:

- Acquaintances

- Friends

- Colleagues at work

- Professional relationships (LinkedIn and professional networking)

- Community

- Family

- Romantic relationships

- Relationship with oneself

You must decide which relationship you want to focus on during each period of life. It will change as you mature and reach different life goals. There are times when it is best to develop oneself, while other times you may want to work to build a community around you where you live.

Find Ways To Monetize Your Passion

Jobs come and go, but you may never be out of work if you can find ways to monetize your passion. You will also enjoy work and want to do it each day. The Internet has made it easier to discover your interests. You no longer need to go to college, study, get a degree, and hope it works out. You can learn from people online by watching videos and purchasing digital courses.

You can then work to build your online presence. Build a business around a passion in a niche. People may eventually find you. You can then make money from:

- Advertisements

- Merch

- Digital products

- Physical products

- Services

- Subscriptions

- Royalties

Secure Single recommends:

-

15 Habits To Build Wealth For Singles

-

Ways To Save Money At The Grocery Store During Inflationary Times

-

Singles Do Not Need An Artificially Intelligent Boyfriend Or Girlfriend

Summary

Self-investment is the best investment you can make. Focus on your health, learn to cook, master the basics of personal finance, cook for yourself, prioritize your health, develop relationships, and work to monetize your passion.

Views expressed in this article are opinions of the author and do not necessarily reflect the views of Secure Single. James Bollen is the author of Thriving Solo: How to Flourish and Live Your Perfect Life (Without A Soulmate). Now available in paperback on Amazon. Subscribe to Secure Single’s Substack for free!

Have you noticed prices going up at the grocery store? You are not alone in seeing the rising prices. Here are seven ways to save money at the grocery store during inflationary times.

7 Ways To Save Money At The Grocery Store During Inflationary Times

Write A Grocery List

You want to enter the grocery store with a grocery list. A grocery list helps you to stay organized. You can include on the list the necessities that you need to purchase. This will help you to save money. Only buy the items that are on your grocery list.

Wants Versus Needs

You want to differentiate between wants and needs at the grocery store. Do you really need the six-pack of beer? Or is that a want? You can purchase the essentials you need to live each month. That means buying the items that you need each month. You can purchase only the basic things that you need to cook.

Purchase The Store Brand

You can purchase the store brand instead of the name brand. The store brand is cheaper compared to the name brands. This is a way for the grocery store to make more money when you purchase the store brand product. It will also save you extra money. It is a win-win for both parties. Sometimes, the store brand may be just as good as the name brand.

Do Not Let Your Food Go Bad

Do not purchase more food than you will eat because then the food will go bad. That is food that you will throw into the trash can. The United States wastes roughly 120 billion pounds of food each year. This is another way to save money. Food that goes to waste is bad for your wallet. It is also food that goes to trash and into the landfill. Save money by only purchasing the amount of food that you will consume when you go grocery shopping.

Shop Sales

You can shop the sales at the grocery store. You can read online what the store may have on sale this week before you go to the grocery store. You can see what is on sale when you go to the store. Rather than purchasing what you had intended to purchase, you could buy the substitute that is on sale. That may slightly change your recipe for when you cook, but it will save you money.

Buy Meat On Special

You can purchase meat when it is on special. You can get decent discounts when you buy meat on special. For meat, it will be somewhere around the store’s meat section. Meat is one of the most expensive grocery store costs. You can sometimes find good cuts of meat on a discount, but you must cook it that day or the following day., It would be best to use your judgment for whether the meat is close to going bad or still good.

Do Not Shop Hungry

You want to avoid entering the grocery store hungry. Make sure you shop on a full stomach. You may purchase more items than you intended to because you were hungry. You may buy some of the stores prepared food. You could cook the same equivalent meal for less at home.

Secure Single recommends:

- How To Be Single In 2023

- The Power Of Going Your Own Way

- How Mindset Affects Success

- How To Use Failure As A Learning Experience

- 15 Habits To Build Wealth For Singles

Conclusion

This is a list of ways to save money at the grocery store during inflationary times. You can work to start to change your shopping habits to save more money while shopping. These are also great ways to save money, no matter the current economic climate. Change your shopping habits. Save money.

James Bollen is the author of Thriving Solo: How to Flourish and Live Your Perfect Life (Without A Soulmate). Now available in paperback on Amazon. Subscribe to Secure Single’s Substack for free!

Are you worried about a recession? You cannot control what happens in the economy, but there are certain things you can control. Here are seven strategies for singles to survive a recession.

Strategies For Singles To Survive A Recession

Signs Of A Recession

Are we in a recession? Go Banking Rates lists ten common signs of a recession:

- More people can’t pay their loans.

- Taxes bring in less revenue.

- Rapid increases in fraud rates.

- Oil price shocks.

- Rising interest rates.

- Decreasing home prices and sales.

- Declining prospects for bellwether companies.

- Stock market crashes.

- Unemployment rates drop too low.

- Inversion of the yield curve.

Those are just some common signs to be aware of to determine if we are in a recession. The prices at the grocery stores and gas stations continue to rise. Another option could be that we have an inflationary recession. That would mean that, along with the regular recession signals, we would experience inflation. It would be the worst of both worlds.

7 Ways To Survive A Recession

Save Money

You want to make sure that you have money saved. Most Americans do not even have $1,000 saved in an emergency fund. You will be ahead of most Americans simply by having money in a savings account. Once you have enough money saved, you can start investing in assets.

Precious Metals As Insurance

Once you are comfortable with the money in your savings account, you can decide to save a percentage of your money in precious metals. Precious metals are a form of financial insurance. It is generally recommended to have ten to fifteen percent of your net worth in precious metals. This is simply a way to diversify outside of a currency and into a hard asset.

Physical precious metals are often considered lifetime investments to be passed down to the next generation. If you want to invest in precious metals that are more liquid, you could invest in precious metals ETFs.

Negotiate A Raise With Your Employer

You could negotiate a raise with your employer. This means they may be unwilling to negotiate with an employee who wants their wage or salary increased. There are seven steps to negotiate a raise:

1. Research data for your current position.

2. Review the company’s financial performance.

3. Reflect and list your achievements.

4. Figure out what your target range is a raise.

5. Prepare a presentation to your employer.

6. Practice your negotiation skills first with your friends and family.

7. Schedule a meeting to negotiate for a raise with your employer.

The difficulty with doing this during a recession is that many employers will look for ways to reduce and cut costs. Employees will often be the first on the chopping block.

Get A Second Or A Third Job

You could get a second or third job to make more money. This may work, but you are still trading your time for money. You can only work so many hours in a day or week.

You may get away working multiple jobs at a time, but eventually, it may negatively affect your health and personal life. You could decide to look into side hustles.

Start A Side Hustle

You could start a side hustle. You could start a side hustle to turn it into a new revenue stream. When looking at side hustles, consider ones you can turn into a passive income stream.

Some everyday side hustles that are active income streams or other jobs include Uber, freelancing, or being a virtual assistant.

Some side hustles that could turn into passive income are starting a YouTube channel, writing a Substack newsletter, or writing eBooks.

Build Passive Income

The beauty of passive income is that it pays you while you sleep. Your paycheck from your employer is active income. You are trading your time for money. You can only work so many hours in a day. It has been found that the average self-made millionaire has a minimum of three passive income streams.

There are many ways to build passive income streams in the Internet Age. You want to learn to play to your strengths. You can then decide if you want to set up a business to be a financial asset to protect your passive income streams.

Start An Online Business

You can start an online business. A business is the ultimate financial asset because you can build it to be as large as you want. You can create as many products and services as you want for customers. You can then pay yourself through your business each month.

You built the business. You can then pay yourself for the hard work to make it once it generates revenue and eventually a profit. Some ways that you create revenue streams for an online business are:

- Advertising on a website, YouTube, or other social media.

- Sell merchandise.

- Sell physical or digital products like PDFs or books.

- You can sell products on a third-party company like Amazon or Etsy.

- You can find ways to earn royalties.

- Provide a consulting or coaching service.

- Sell a premium newsletter and have premium articles on a website.

You are your own limit when you are responsible for a business. You can also find creative ways to make more money with a business.

Secure Single recommends:

- Introduction For Singles On The Different Types Of Savings Accounts

- How Mindset Affects Success

- How To Be Single In 2023

- 15 Habits To Build Wealth For Singles

- 12 Reasons Why Young People Should Not Go To College

Summary

It is up to you to take action to prepare for a recession. These are just some strategies for singles to survive a recession. Whether you think there will be a recession or not, it is always a good idea to be prepared. One of the ways to be prepared is to save money and find ways to increase your income.

Views expressed in this article are opinions of the author and do not necessarily reflect the views of Secure Single. The content is intended for informational and educational purposes only. Subscribe to Secure Single’s Substack for free to receive more content like this directly in your inbox.

There are different types of savings accounts. Savings accounts play a crucial role in personal finance and building wealth. Here is an introduction for singles on the different types of savings accounts.

Introduction For Singles On The Different Types Of Savings Accounts

What Is A Savings Account?

You can earn interest with the money you deposit in your savings account at a financial institution. A savings account is a good choice to leave cash for your short-term needs. There are different types of savings accounts.

A savings account can accrue interest daily, monthly, quarterly, semi-annually, or annually. You will want to check with the financial institution to understand how often it will compound interest.

You will always want to check with the financial institution where you are saving your money to ensure you are not penalized if you exceed their minimum amount.

A savings account is best used for short-term to medium-term financial goals.

Standard Savings Account

You can open a basic savings account when you open a checking account at a bank. A regular savings account will pay you less than other options. But you can automatically set up your checking account to send money to your savings account each month. This is an easy way to build up your savings.

You can keep three to six months of money in a regular savings account. This can help you to cover your everyday financial expenses in your checking account.

High-Yield Savings Account

A high-yield savings account provides a higher interest rate than a standard one. A high-yield savings account can pay you up to twelve times more than a standard one. The bottom line is you will earn more interest by putting some of your money away in a high-yield savings account.

A high-interest savings account is an excellent choice for saving your emergency fund money. This is because it earns you higher interest. It is recommended to have a minimum of $10,000 for an emergency fund. You can tailor your emergency fund goal using Nerd Wallet’s emergency fund calculator.

Money Market Account

A money market account is yet another type of savings account. A financial institution may refer to the account as a money market account (MMA) or a money market deposit account (MMDA).

Money market accounts also offer other features that a regular savings account does not provide. These features include higher interest rates, check-writing, and debit cards.

Certificate of Deposit (CD)

Another savings tool at your disposal is the certificate of deposit (CD). A certificate of deposit earns interest on an agreed-upon percentage rate between you and the financial institution. You cannot touch the money in a CD until maturity, or you will be penalized. The tradeoff for a higher interest rate is less liquidity compared to a savings account.

A certificate of deposit can range from seven days to a few years. The interest rate that is offered will vary for each term length. You will want to research by looking at financial institutions where you live and online to find who provides the best rates and fits what you are looking for with a certificate of deposit.

Solutions

You can make it a habit to save a certain percentage of money each month to build up your savings accounts. The 50/30/20 budget recommends saving a minimum of twenty percent each month. Saving is a financial tool that can help you deal with financial emergencies and invest in other assets.

Once you have saved enough money, you can invest money in:

- The stock market.

- Real estate.

- Start a business.

- Commodities.

Secure Single recommends:

- Self-Validation For Singles

- Anti-Dating: Dating Is Not The Answer For Singles

- 30 Ways To Make The Most Of Being Single Today!

- 15 Habits To Build Wealth For Singles

- 15 Ways To Have A Thriving Social Life As A Single

Summary

You have many choices when it comes to savings accounts. It ultimately depends on your financial goals and where you are in your financial journey.